When it comes to estate planning, co-ordination of documents and details such as beneficiary designations matter. A lack of planning and out of date or incomplete documentation can result in additional costs, delays and taxes for your estate, or a loss of control over certain aspects, such as the guardianship of minor children and/or how you want your assets to be distributed when you die. Even carefully planned estates can be undone by technical glitches or unnecessary complications.

What is an estate1?

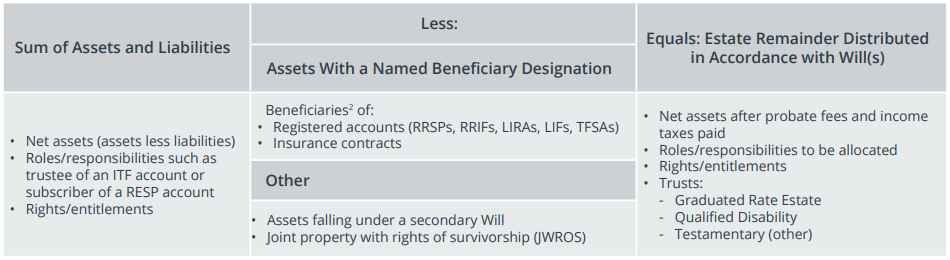

An estate is the net worth of a person, namely: the total value of your assets, including any legal roles, responsibilities, rights, and entitlements you may have, minus assets flowing directly to your beneficiaries and any changes to your legal standing, as outlined in Table 1.

Table 1: The Estate Equation

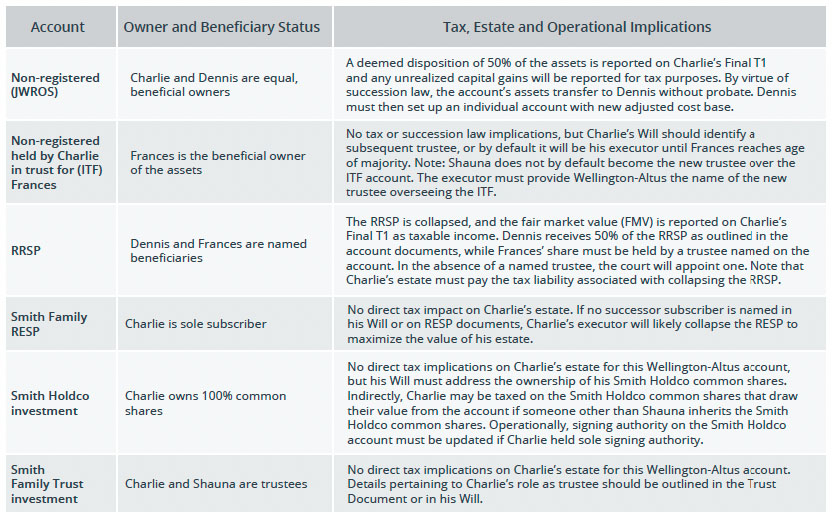

Your Wellington-Altus investment accounts

When you die, the assets in your various Wellington-Altus accounts remain invested until they are transferred to beneficiaries named in the account documents or your executor acts on the instructions you have provided in your Will.

Upon notice of death, purchases in non-managed accounts are restricted, dispositions are allowed and any outstanding or closing fees will be charged. There are no trading restrictions on managed accounts and fees will be charged until assets are transferred and the estate is settled.

To facilitate the transfer of wealth, here are some key estate planning points to consider: