“Vincit qui patitir.” – Latin proverb

(Rough translation: “He who endures will conquer.”)

After a year that few could have predicted, we look forward to a year that, for many, couldn’t have come soon enough. For 2021, we forecast another good year for risk assets. By the end of 2021, the S&P 500 has the potential to test the 4,500 level and global corporate earnings will be strong.

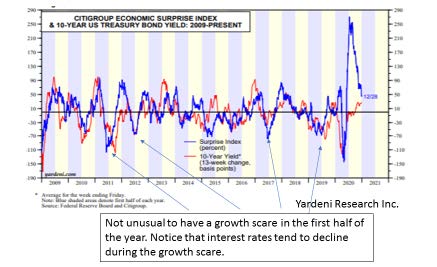

To be clear, there will be bumps along the way. Our base case posits that the first half of 2021 will be constrained by an economic growth scare with increased volatility. This should cause a healthy correction in equity markets and a decline in long-term interest rates. As with every year, a correction of between 10 to 15% should be expected. Using 2010 as a guide, when investors questioned the sustainability of the bounce off of the 2009 low, after a brief correction in early 2010 the business cycle kicked in generating an opportunity for investors to capture above-average returns. We see 2021 closely following this 2010 analogue.

After a growth scare captured in the first half of the year, we expect a continuation of the “V-shaped” recovery which started in late April 2020 and strong earnings growth (25 to 30%) to influence the latter half of 2021. As we saw in 2020, bullish sentiment continued to build throughout the year, reaching extreme levels to end 2020 and hitting our 2020 S&P 500 target of 3,700. We expect Wall Street to similarly play catch up by year end.

Citigroup Economic Surprise Index & Yield on U.S. 10-Yr. Treasury Bond

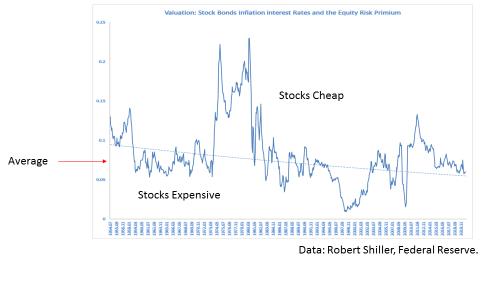

Fair Value Today…But Be Prepared

In 2021, global policymakers will make continued and significant efforts to support economic growth by fiscal and monetary means; do not fight it. This will stimulate GDP growth, expected to be close to 6% by year end. Corporate profit margins and earnings growth will accelerate and inflationary expectations will continue to increase, steepening the yield curve, thereby helping risk assets to appreciate. When one takes into consideration interest rates, inflationary expectations, dividend yields and the earnings growth of the S&P 500, our model agrees with the current position of Chairman Powell: stocks look to be fairly valued on a long-term historical basis.

Given the desire of central bankers to anchor interest rates at close to zero, and with a reacceleration of the global economy increasing inflationary expectations, one should expect stock valuations to become expensive over the next few years. Valuations across certain asset classes are, in some cases, at historical extremes; undervalued assets that are, on a historical basis, cheap relative to growth will significantly eliminate this undervaluation in 2021. Investors should consider applying elements of the early cycle playbook when constructing portfolios: U.S. and European financials, cyclicals, materials and segments hard hit by the Covid-19 lockdowns, now aptly termed the “epicenter stocks,” such as travel and leisure, should perform well.

Historical S&P 500 Valuation

The Great Reset: Real & Profound

In 2021, the global economy will continue to evolve from analog to digital and leading technology stocks should perform well, particularly in the first half of the year. History suggests that natural disasters – including the unanticipated pandemic we are experiencing – accelerate and amplify the evolutionary trends that already existed in the economy prior to the disaster. To that point, there is no “normal” to return to, thus as the economy opens after a brief cyclical spurt a new post-Covid-19 economy will be upon us. To be clear, this reset is real and profound. Investors need to keep an open mind; what we have maintained to be status quo, largely developed post World War II, will be challenged and replaced.

An Opportunity? The Great Reset of Our World

Longer-Term Themes Driving 2021 & Beyond

Driving our view for 2021 and beyond are the following longer-term trends:

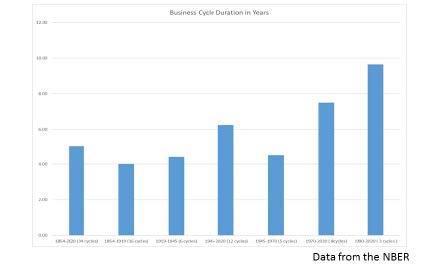

We are in the early stages of a new business cycle. This could last another eight years. The global economy is going through extreme structural change, akin to that which is experienced every 80 years. We are at the onset of this great reset. Recall a lesson from history: As the world emerged from World War II, many were concerned about deflationary pressures and the possibility of economic growth severely contracting. Global policymakers developed rules, institutions and programs aimed at generating economic growth in a non-deflationary environment. Today, the global economy faces the same dilemma. Policymakers are using the opportunity created by the pandemic to redirect and refocus the global economy for decades to come.

Business Cycles From 1854

Demographics have changed. Millennials and GenXers are driving investment preferences, consumption patterns and social norms. In 2021, the oldest millennial will be 40 years old. Today, more than half of the U.S. population is the age of the millennial generation or younger, overtaking the Baby Boomer segment – the predominant demographic since the late 1980s.

The death of globalization continues. The rivalry between China and the U.S., evident in economics and technology, will persist and intensify. Populism will continue to fuel economic nationalism accelerating the on-shoring of supply chains and competitive devaluation of currencies – perhaps, culminating in the negotiation of a new Bretton Woods movement. The deflationary forces caused by the addition of low-cost labour from Asia and Eastern Europe has now run its course and is reversing. Extreme levels of global debt will force policymakers to make generational changes or suffer the consequences of the risks evolving from liquidity to insolvency. Europe needs to implement structural reforms; China needs to open its economy to foreign capital flows and freely float its currency.

Digitization dominates. The pandemic has accelerated and amplified the digital evolutionary process, forcing almost every industry, government and company to adjust. The platforms initially built in the late 1990s,

during the technology, media and telecom (TMT) bubble, have acted as a springboard to usher in a period of intense creative destruction: a new, decentralized digital internet platform focused on data security based on blockchain; manufacturing platforms built on robotics, machine learning and alternative intelligence; healthcare platforms built on DNA sequencing; and communication platforms built using 5G. In the next decade, a staggering 65% of global GDP will undergo a digital transformation. This means that many companies and industries that make up the S&P 500 will face extreme pressure to evolve or face potential extinction.

The financial markets are not immune to this evolutionary change. With the rise of passive investing, the internal structure of capital markets has been significantly altered, increasing the likelihood of extreme market swings. However, the pivot by central bankers to focus on inflation targeting and targeted credit creation – including in the Green Economy – will provide opportunities for investors, supporting economic growth and reshaping the global economy during these early days of the new business cycle. We continue to see evidence of the migration towards the new tomorrow; in the digital transformation, blockchain and digital assets continue to be increasingly accepted within mainstream financial circles.

Even the vehemence of an unanticipated global pandemic wasn’t enough to derail our 2020 forecast, but, as in any year, surprises can happen in 2021 that may cause adjustments to our base case investment thesis. While the most obvious is the potential for the global economic reopening to be much slower – or faster! – than the market currently believes, investors should also be prepared for changes that may be quietly taking shape behind the scenes:

- Rapidly rising inflation forces central bankers around the world to tighten credit conditions, raising interest rates earlier and faster than the market expects and creating the likelihood of a solvency debt crisis.

- China’s economy collapses under extreme levels of debt: is the day of reckoning looming?

- In the U.S., a new constitutional crisis emerges focusing on the roles of the U.S. Supreme Court and Federal Reserve.

- China, Europe and U.S. policymakers focus on breaking up the big tech firms.

- Under its new direction, the U.S. implements socialist economic policies.

- The U.S. and its NATO allies continue to further isolate China and Iran, with the possible use of force.

One year ago, much seemed right with the world – then, we quickly learned all that could possibly go wrong. Yet, 2020 taught us that, despite immense hardship and tragedy for many, the human race has the remarkable ability to endure. For 2021, investors should expect volatility in the first half of the year, due to stagnating progress in the fight against the pandemic. As growth concerns are alleviated, however, anticipate an acceleration of economic growth and a strong rally to year end. As we write the next chapter, don’t overlook the endurance that brought us to today as it will likely be an asset to carry us through the year ahead.

James E. Thorne, Ph.D.