Les clients qui ont transféré leur régime enregistré d’épargne-retraite (« REER ») dans un fonds enregistré de revenu de retraite (« FERR ») ou qui avaient déjà un FERR en 2023 trouveront ci-dessous des renseignements leur indiquant comment leur retrait minimum sera calculé pour 2024. Tous les retraits d’un FERR sont déclarés à titre de revenu de pension sur un feuillet T4RIF.

Voici quelques règles de base concernant les FERR:

- Les retraits d’un FERR doivent commencer la première année civile suivant l’année de l’établissement. Aucun retrait n’est exigé dans l’année où le FERR est établi.

- Chaque année, un rentier de FERR doit retirer un ou plusieurs paiements égalant ou dépassant le montant minimum calculé. Ce montant est fondé sur les facteurs suivants:

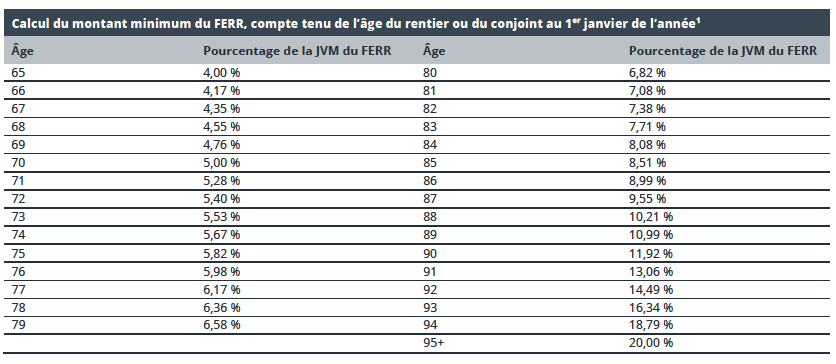

- La juste valeur marchande (« JVM ») du FERR au début del’année civile. À des fins pratiques, la JVM de clôture dudernier jour ouvrable de l’année civile précédente estutilisée. Pour 2024, ce jour tombe le 29 décembre 2023. La JVM du FERR est ensuite multipliée par lefacteur/pourcentage correspondant à l’âge du rentier.

- Le calcul peut utiliser l’âge du rentier ou de son conjoint au 1er janvier. On doit décider quel âge utiliser au moment du premier retrait du FERR et ce choix est irrévocable. En général, il est préférable d’utiliser l’âge le plus bas, car cela permet d’obtenir un montant minimum inférieur. Il est toujours possible de retirer des fonds supplémentaires au besoin.

- Si l’âge choisi est inférieur à 71 ans, la formule suivante sert à déterminer le pourcentage utilisé pour calculer le montant minimum :

1 Pour les FERR établis après 1992

- Le montant minimum de retrait ainsi calculé n’est pas assujetti aux retenues d’impôt. Tout retrait d’un FERR excédant le montant minimum calculé est assujetti à des retenues d’impôt, selon la province de résidence et le montant du retrait excédentaire. Les taux de retenue d’impôt suivants s’appliquent :

- Vu qu’aucun retrait n’est exigé au cours de l’année d’établissement du FERR, tout versement du FERR au cours de la première année civile est assujetti à une retenue d’impôt.

- Les FERR n’ont pas de montant limite de retrait maximum autre que la JVM du FERR.

Application des règles

Pour comprendre comment fonctionne le calcul du montant minimum du FERR, examinons quelques scénarios:

- Jordan a eu 65 ans en 2023; il a pris sa retraite et a converti son REER en FERR. L’épouse de Jordan, Meghan, a 66 ans.

Au début de l’année, la valeur du FERR de Jordan est de 600 000 $. Quel est le montant minimum du FERR de Jordan pour 2024?

- Vu que Jordan est plus jeune que Meghan, son âge serait généralement utilisé.

- Étant donné que Jordan avait 65 ans le 1er janvier, le montant minimum qu’il doit retirer de son FERR en 2024 correspond à 4 % de 600 000 $, soit 24 000 $.

- En gardant les mêmes hypothèses que dans le scénario 1, mais en faisant passer l’âge de Meghan à 63 ans, quel serait le montant minimum calculé pour le FERR de Jordan?

- Étant donné que Meghan est plus jeune, son âge serait généralement utilisé dans le calcul du montant minimum et diminuerait le pourcentage du montant minimum du FERR de Jordan comme suit : 1 / (90 – 63) = 3,70 %.

- Ainsi, le montant minimum devant être retiré du FERR de Jordan en 2024 correspondrait à 3,70 % de 600 000 $, soit 22 200 $.

- Si Jordan et Meghan ont tous les deux 78 ans et que le FERR de Jordan a une valeur de 500 000 $ au début de l’année, quel serait le montant minimum calculé pour le FERR de Jordan en 2024?

- 6,36 % de 500 000 $, soit 31 800 $.

En conclusion

Cette communication explique comment le montant minimum des retraits de FERR est calculé. Il y a quelques situations où les clients peuvent souhaiter retirer plus que le montant minimum de leur FERR. Par exemple, ils peuvent vouloir suppléer à leur revenu en fonction de leur taux marginal d’imposition ou fractionner le revenu de pension admissible avec leur conjoint et utiliser des taux marginaux d’imposition plus bas.

Pour obtenir de plus amples renseignements sur ces options et d’autres occasions de planification fiscale, veuillez communiquer avec votre conseiller de Wellington-Altus.