Passing the Peak Sagitta of the Inflation and Rate Expectation Arcs in 2022

“Let us do something while we have a chance! It is not every day we are needed.” — Samuel Beckett, Waiting for Godot

Investors are waiting for their own Godot – certainty about the future. Like Godot, that certainty never comes. Yet, we keep waiting for it, even with a highly levered global economy that’s experienced two exogenous shocks. Central bankers are concerned that inflationary expectations will become unanchored. They have embraced a historic tightening cycle with aggressive interest rate hikes and contraction of balance sheets. We don’t know the slope of the arc’s downward trajectory and glide path. The sagitta is the height of an arc segment, its peak, and my non-consensus view is that we are past the sagitta for inflation and peak tightening expectations. We expect more data to support this view throughout the fall and into early winter. Unfortunately, investors will have to wait for it.

The risk of a hard landing or even a global credit event continues to be front and center. For investors, in the short term, the Godot moment will be when the economy strings together three or four months of declining economic growth, falling prices and the central bank’s response. Will central bankers continue to raise rates, creating a deep recession or even a global credit event? With headline inflation at historic levels, the need and pressure to do something is immense. But are central bankers doing too much?

As of writing, the answer is no. They’ve done a heroic job. The economy is slowing, job openings are declining, wages are falling, the housing market has rolled over, commodity prices are down, and month-over-month price readings in some areas are deflationary. But proclamations that there is no other option than to aggressively raise rates should concern investors. There is another alternative: patience and prudence. But are central bankers going to snatch defeat from the jaws of victory, as they lose patience waiting for Godot to arrive? To be clear, as in Beckett’s play, certainty about the future will never come. But for investors, it’s how policymakers respond to this uncertainty that is so important.

To be sure, we must continue to endure a cacophony of Federal Reserve officials communicating formal proclamations about their focus on price stability and the magical 2% target. Get ready for the new drumbeat of “higher for longer” to become the mantra of many pundits, just as the prices of used cars early this year was used as a mantra for permanent inflation. According to Bespoke Investment Group, wholesale used car prices are down 10% in 2022. This price decline has yet to be priced into the retail used car market where it might show up in inflation data. To wit, price declines will take time to show up in yearly data, supporting our thesis that we are past the peak in inflation.

The hidden lead in this narrative is no one knows what willhappen next. How quickly will the economy decelerate? What will be the composition of growth? Will it be above or below trend? Will inflation fall back to 2%, or will it be structurally higher? What is the correct terminal interest rate, the long-term non-inflationary level of employment, and the long-term scarring effects of COVID-19? How will the war in Ukraine be resolved? Is the growth miracle of China over? No one knows the answers to these questions — the Bank of Canada, the Federal Reserve, or anyone on Wall Street or Bay Street, including your humble servant. We don’t know. What’s concerning is that many think they do know and are certain that their forecast is correct. As Mark Twain wrote, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that ain’t so.” My concern is the loss of patience by policymakers. Gandhi teaches that “to lose patience is to lose the battle.” In my opinion, policymakers are losing their patience.

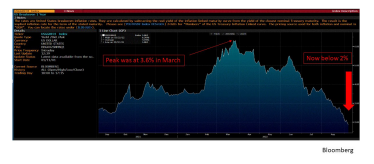

This concern was reinforced by the tone and message of U.S. Federal Reserve (Fed) chairman Jerome Powell’s speech this year at Jackson Hole and the certainty of all participants that this is the right path as we embark on an uncertain journey fraught with danger. Ignoring the fact that inflation expectations, long and short, have declined. According to Bloomberg, the one-year inflation breakeven, which peaked in March at 3.6% has declined and is now below the Fed’s inflation target of 2%.

1 Year Inflation Breakeven PEAK was in March currently below 2%.

To be clear, aggressive tightening into a rapidly slowing, highly levered, uncertain economy is a very high-risk strategy. We hear from policymakers that there are no other alternatives, as we heard in the fall of 2007. How about pausing and letting the markets adjust naturally? Why the loss of patience? Will the hawkish posturing by central bankers continue throughout 2022? We have supported central banks’ measures to control inflationary expectations as we waited for the economy and prices to decline.

My view has always been that the downshifting of tightening needs to start at the September FOMC meeting. Ignore the rhetoric coming out of Jackson Hole; I expect the Federal Reserve is still data-dependent, and the data will allow the Fed to downshift rate hikes. Note that pundits being happy because the speech that Powell gave during his Jackson Hole speech contained the word pain, and the name of Paul Volcker. Investors should assume we have another 100 basis points in hikes in front of them by the end of 2022. Rapid deceleration in prices and wage growth to the 3% range would put this forecast at risk. I also differ from consensus that in the post-WWII era – in my view more relevant than the 1970s – the Fed’s main instrument to control a three-year inflationary spike was achieved through the management of their balance sheet. To be clear, inflation was defeated, and a soft-landing was achieved.

The breaking of a sacrosanct rule

In July, Powell claimed that the federal funds rate was now “neutral.” His inference that the Fed was close to restrictive territory and, therefore, closer to being done tightening was well received by the global financial market. But the Fed’s critics went apoplectic, as both former Federal Reserve Bank of New York president William Dudley and former Treasury Secretary Larry Summers broke the holy rule of insiders criticizing insiders in public. Summers criticized Powell for engaging in “wishful thinking.” Investors note that the official sector is not a monolith, and many still evaluate the world through a 1970s lens. Our financial markets have changed; markets react quickly to the moral suasion of the communication strategy of central bankers. Once the Fed initiated its hawkish communication pivot, the long end of the yield curve marched higher, and mortgages increased from 3% to 6% by July this year, the beginning of the aggressive tightening cycle.

Mortgage Rates have already doubled!

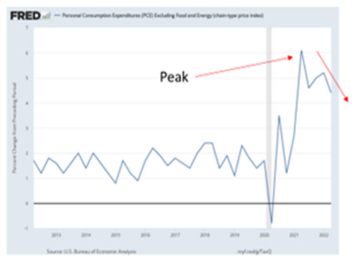

The housing market is already in recession, yet Dudley and Summers conveniently omit this from their attack on Powell. How can tightening financial conditions in the housing market not be considered if the Fed employed a holistic interpretation of the financial conditions of an economy? But to the point of order, Summers does have a point. With the Core PCE August reading declining to 4.4% after peaking earlier in the year at close to 6%, the short-term terminal rate should be higher. The long-term terminal interest rate of 2.5% assumes Core PCE is in the 2% target range. If Core PCE is higher than 2%, the terminal interest rate should also be higher. Where does inflation settle out? We don’t know. We know the market expectation of inflation one year out is below 2%. If these expectations are correct, then in a year, Core PCE should be dramatically lower, and then Powell’s July statements may have been accurate, and all the criticism misplaced. To be sure, we don’t know the new terminal interest rate. But the subtle point many investors miss in this discussion about where rates should be, is that the determining factor is Core PCE and not headline inflation. Investors should also note that Dudley and Summers were delighted with chairman Powell’s Jackson Hole speech. Not a surprise.

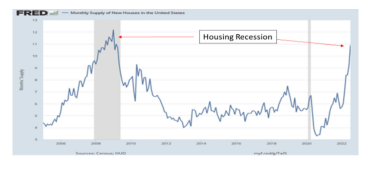

Housing Inventory levels at 2008 levels.

Critics are also ignoring the generational valuation levels of the U.S. dollar (USD). A strong USD is deflationary and tightens financial conditions. I can easily make the case that the strong USD is equivalent to at least a 50-basis-point (bps) rise in the federal funds rate. Lastly, the Fed has just started its quantitative tightening program to contract its balance sheet, which the Federal Reserve used in the late 1940s to crush three years of average inflation of over 10%. As recently as October 1, 2020, Dudley, while at the Fed, voted for the second round of quantitative easing (QE), proclaiming that a QE of $500 billion was equivalent to 50 to 75bps of cutting the Fed Funds rate. So, by my math, considering the value of the USD (50 bps), reducing the balance sheet by $500 billion (50 to 75 bps) plus Fed funds at the current levels, the equivalent Fed funds rate would be at least 100 bps higher. This back-of-the-envelope math leads me to conclude that we are closer to the end of the tightening cycle than the consensus believes. The real question is do central bankers take a non-holistic view when calculating what the neutral rate should be? If data continues to fall the right way, capital markets will discount the downshifting of interest rate hikes, and risk assets should appreciate as they did in the 1994-95 mid-term election year.

We are past the peak sagitta of “the arc” for inflation and rate tightening expectation

Contrary to reports in the media, economic data is starting to turn. The pace of declining inflation is unknown. We don’t know the glide path. Is it steep, gradual or does it level out after a period of decline? To be sure, drivers for accelerating inflation have dramatically declined, the housing market and inventory levels are at the highest since the 2008 crisis, and durable goods such as cars and furniture are seeing demand and prices fall. The reverse bullwhip effect affects inventory levels, causing many firms to cut prices. Yes, deflation in some durable areas is starting to show up in the data. Commodity prices have declined significantly. Wholesale gasoline prices are down 38% since June. Indeed.com, a website that tracks job openings in real-time, reports that job openings are down 40% from the peak of this year,

which is significantly more than what JOLTS (Job Openings and Labor Turnover Survey) data reflects. A close look at the employment data reveals that the number of people considered out of the labour force but looking for a job is greater than the number of unemployed workers. Wage growth is beginning to drop, and the fears about a wage spiral episode will be proven to be misplaced.

Inflationary expectations are well anchored. What we are lacking right now are policymakers with patience. For whatever reason, there is a belief that the data we are witnessing is inaccurate and not sustainable. The critical question for investors is will central bankers continue to ignore the turn and aggressively tighten the economy into a severe recession. I believe markets are pricing in rate cuts in 2023 because of the concern that the Fed will do what it has always done and tighten into a recession. Monetary policy is a blunt instrument; the groupthink certainty and belief that policymakers must continue and pile on aggressive rate hikes (and that it’s their only option) is a concern.

Core PCE Peaked in February 2022.

Bullard rightly suggests that today the economy quickly adjusts. But reading Fed speeches and listening to pundits, the quick adjustment is a one-way street. We are in a new economy where adjustments are more rapid. The credit market tightened quickly to the Fed’s communication strategy, and the housing market began to roll over before the aggressive Fed tightening phase; it is fair to assume the lag in which monetary policy affects the economy has declined. However, unlike the Fed and the Bank of Canada, we believe the economy also quickly adjusts when decelerating. Adjustments that happen faster are more intense. Regional Fed surveys, GDP and PMI numbers point to a dramatic deceleration in economic growth. The prices-paid component of the July ISM survey has significantly declined since the late 1940s. Month-over-month data suggests a hard turn is upon us. Core PCE peaked in February. High-frequency employment data and the household survey point to a significant slowdown in the jobs market.

The adjustment process in this new digital economy is symmetrical and a two-way street. Policymakers’ implicit assumption is that the economy’s reaction function is asymmetrical, rapidly adjusting one way and slowly the other. I disagree and believe the data will bear this conjecture out.

The Fed assumes they can continue tightening aggressively and not create a credit event. They made the same assertions in 2008. We are not so sure. Unfortunately, given the chairman’s speech at Jackson Hole, one could easily infer that policymakers have learned nothing from the Great Recession. To be clear, we don’t know, but aggressive actions in times of uncertainty in a highly leveraged global economy are dangerous.

The risk of credit events has increased. Strong dollar era is typically accompanied with crisis emanating from the emerging markets. Given the fragile situation in Europe and China, continued aggressive tightening may ignite a financial crisis as it did previously in Mexico and Asia. Specific to Canada, our economy is not as diversified as the U.S.A., and over-reliance on real estate and energy implies that it would be folly for the Bank of Canada to embrace the same tightening strategy as the Fed.

What should investors do?

As I recommended in June, my high-conviction trade was buying government bonds at the long end of the yield curve. We also recommended investors use the volatility of the summer market to add to high-quality equity secular growth names that perform well in a slow-growth environment. After the significant correction in energy stocks, we also recommended investors consider this sector a secular growth sector. In addition, adding high-quality energy names to take advantage of the price differentials between North America and Europe should be considered. Finally, I will continue to recommend adding to companies that benefit from the transition to net zero emissions, another secular theme.

We are closer to the end than the beginning of this tightening cycle; the month-over-month data continues to point to the fact we are past peak inflation and expectations of interest rate hikes. Just like in Beckett’s play, we are all waiting for Godot — the data — and this time he’s going to show up.

— James E. Thorne, Ph.D.

[1] The height of the arc of a circle.

[2] Adults in the Room, Yanis Varoufakis, 2017.